OpenAI's Leaked Finances: Is the AI Bubble Bursting?

In June 2026, OpenAI's audited financial statements leaked — and the numbers behind the world's most famous AI company turned out to be far stranger than the headlines suggested. If you've seen the "$38.5 billion loss" figure floating around and felt a flicker of either panic or schadenfreude, you're not alone. But that number, on its own, is misleading — most of it is a non-cash accounting charge, not money leaving the building. The real story is more interesting, and it matters for anyone whose savings, job, or career is downstream of the AI boom — which, these days, is most of us.

So here's what we're going to do. Firstly, we'll look at what OpenAI's finances actually say, separating the accounting theatre from the real cash. Secondly, we'll unpack the "circular financing" controversy — the web of deals connecting OpenAI, Nvidia, Microsoft, Oracle, and AMD that has economists using the word "bubble." And thirdly, we'll be honest about what we genuinely don't know. Let's get into it.

What OpenAI's Leaked Finances Actually Show

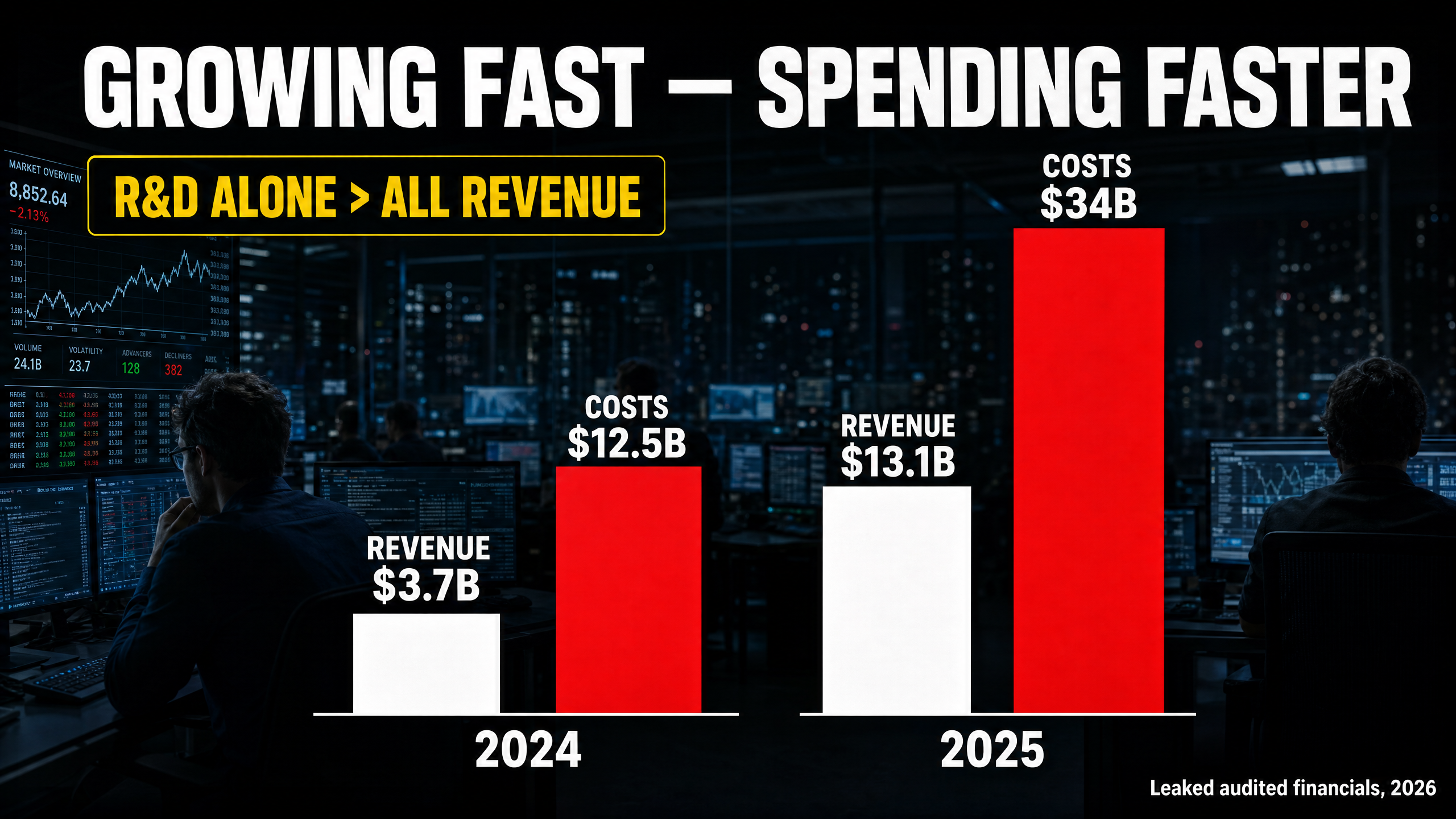

Let's start with the hard numbers, because they're remarkable in both directions. In 2025, OpenAI generated $13.07 billion in revenue — more than triple the $3.7 billion it made in 2024. That's not the growth curve of a struggling company. That's one of the fastest revenue ramps in corporate history.

But the spending grew faster. Total costs hit $34 billion, producing an operating loss of $20.92 billion. Research and development alone came to $19.18 billion — more than the company's entire revenue. Sales and marketing roughly quintupled to $5.73 billion.

Now, the headline you probably saw was a net loss of $38.5 billion. Here's the part most coverage skipped: roughly $41.55 billion of that figure is a one-time, non-cash accounting charge tied to OpenAI's conversion from a non-profit to a for-profit structure. It's not money leaving the building. Strip it out, and the real economic loss is closer to the operating figure — and on a pure cash basis, lower still.

There's even a sign of improving discipline. According to the leaked figures themselves, OpenAI spent $2.37 for every $1 of revenue it earned in 2024, and that dropped to $1.60 in 2025. (Note that's the documents' own efficiency metric, which uses a cash-spend denominator — divide total reported costs by revenue and you get a higher number, because that includes the non-cash charges we just discussed.) Either way, the direction is the same: the company is becoming more efficient as it scales, which is the opposite of what you'd expect from a business in trouble.

One relationship dominates the cost base: of that $34 billion in expenses, $17.2 billion flowed straight to Microsoft for Azure cloud and compute. OpenAI doesn't fully control its own costs — a theme we'll come back to.

The timing of the leak is telling. It surfaced days after OpenAI reportedly filed confidentially to go public with the SEC, with Goldman Sachs and Morgan Stanley said to be leading. (A confidential S-1 isn't public by definition, so this rests on reporting rather than a document anyone can pull up.) Still, the pattern fits: you don't take audited books to regulators if you think they're catastrophic — but you also don't want them leaking on someone else's terms first.

The honest read

OpenAI is burning cash by deliberate strategy, not by accident. Revenue is exploding, unit economics are improving, and IPO money is on the way. The scary headline is mostly non-cash — an accounting charge, not a stack of bills. That doesn't make it meaningless (a fair-value charge on convertible interests reflects real dilution for existing stakeholders), but it isn't cash burning out the door. The genuine risk lives somewhere else entirely — off the income statement.

The Circular Financing Controversy: Where the Real Risk Lives

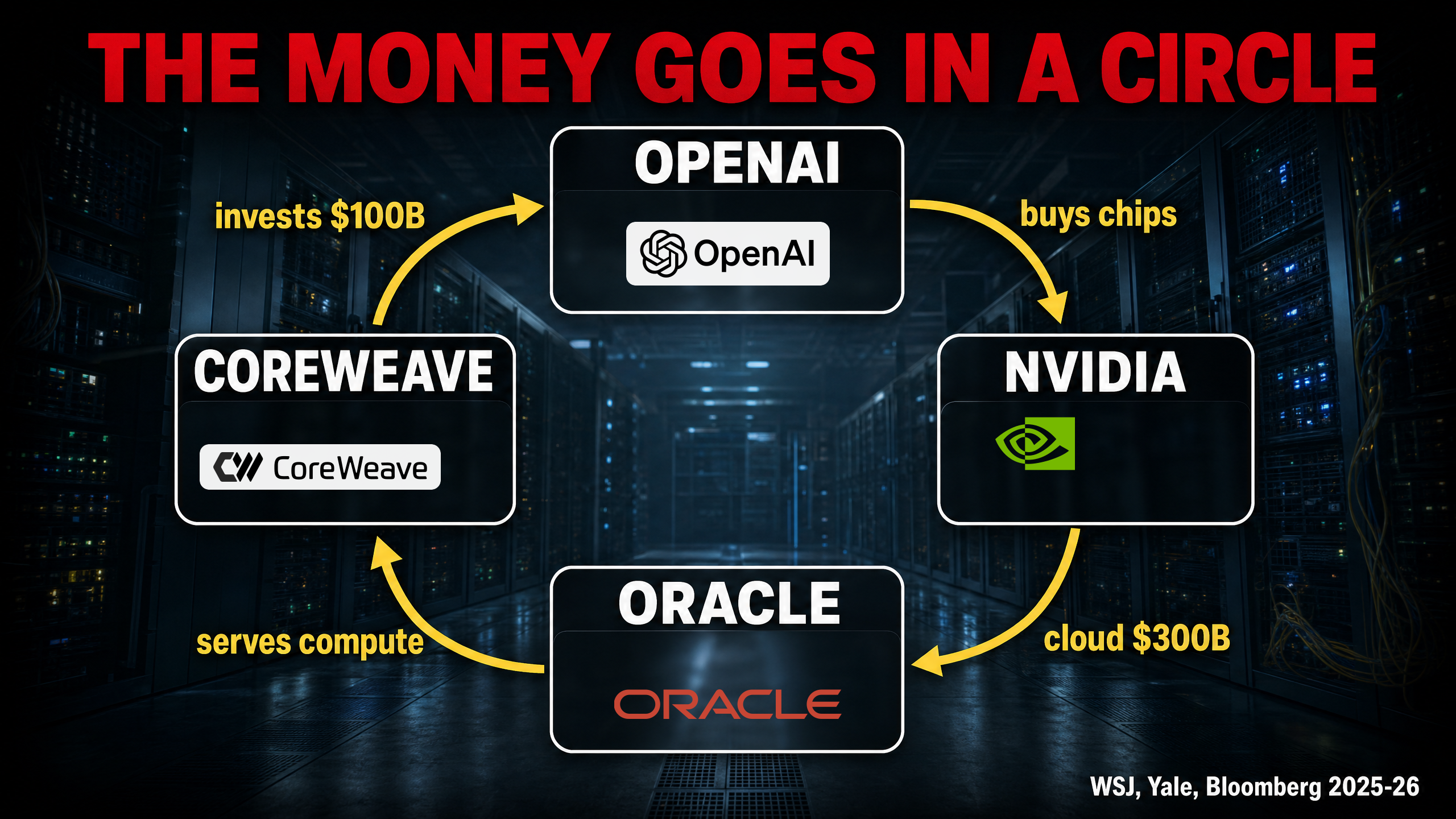

Here's where it gets genuinely concerning, and where the word "bubble" earns its place. OpenAI made roughly $1 trillion in compute and infrastructure commitments across 2025 and into 2026. Set that against $13 billion of revenue and you can see the problem: the company has promised to spend, over the coming years, something on the order of seventy-five times its current annual sales.

But the scale isn't even the most-discussed part. It's the structure. The same companies that sell OpenAI its compute are also investing in OpenAI. Money goes round in a circle.

| Deal | Amount | Direction | Status |

|---|---|---|---|

| OpenAI ↔ Oracle | ~$300B over 5 years | OpenAI pays Oracle for cloud | Reported / announced |

| OpenAI ↔ Microsoft | ~$250B cloud commitment | OpenAI pays Microsoft | Reported |

| Nvidia → OpenAI | up to $100B | Nvidia invests in OpenAI | Announced intent |

| OpenAI → AMD | warrant for ~10% of AMD | AMD gives OpenAI equity upside for buying its chips | Announced, contingent |

| Nvidia → CoreWeave | ~7% stake / ~$6.3B | Nvidia invests in + buys from CoreWeave | Reported |

| OpenAI → CoreWeave | ~$22B | OpenAI pays CoreWeave for capacity | Reported |

The loop critics point to runs like this: Nvidia invests in OpenAI → OpenAI buys Nvidia chips (directly, and via Oracle and CoreWeave) → Nvidia also owns part of CoreWeave → CoreWeave serves OpenAI. Round and round.

Why does that worry people? Two reasons. First, it can inflate the appearance of demand — if a chipmaker funds its own customers, some of that "demand" for chips is really the chipmaker's own money coming back to it. Second, it creates systemic risk. As one analyst put it: if OpenAI can't pay Oracle, Oracle can't pay Nvidia, and Nvidia's stock crashes — and Nvidia is one of the most valuable companies on Earth. The dominoes are wired together.

This isn't a fringe view. Jonathan Weil at the Wall Street Journal asked directly whether the flurry of circular AI deals was a "win-win or a sign of a bubble." Yale's Jeffrey Sonnenfeld and Stephen Henriques wrote a piece titled "This Is How the AI Bubble Bursts," pointing to exactly these tangled equity-and-revenue arrangements. Bloomberg built an entire interactive feature mapping the circular deals.

The defenders have a fair point too, and intellectual honesty demands we state it. A circular deal is not the same as fraud. Round-tripping in the accounting-scandal sense means sham transactions with no real economic substance — and that's not what this is. The compute is real, it gets used, and the customers paying for it are, unlike the dot-com startups of 2000, mostly profitable giants with strong balance sheets. The bull case is simple: if AI demand keeps growing, the whole structure unwinds gracefully and everyone wins.

So which is it? That's the trillion-dollar question — and the honest answer is that nobody knows yet.

Is OpenAI Actually in Trouble?

Let's separate two questions that often get blurred together.

Is OpenAI in trouble today? Probably not. Revenue tripled, the cash burn is smaller than the headline suggests, efficiency is improving, and an IPO is about to refill the tank. A company can lose money for years and be perfectly healthy if it's choosing to spend on growth and the growth is real. OpenAI's CFO has said publicly the company could break even if it wanted to. The losses are a decision, not a death spiral.

Is the bet in trouble? That's the live question. The ~$1 trillion in commitments only makes sense if OpenAI's revenue reaches the projected scale — figures of around $200 billion a year by 2030 have been reported, with cash-flow positivity targeted around 2029–2030. If that curve materialises, the structure holds. If AI demand or pricing disappoints, the commitments don't shrink to match.

That's the real shape of it: not a company about to collapse, but a colossal bet that only pays off if the growth story stays true.

What This Means for You

You might be reading this thinking, "I don't own OpenAI shares, so why should I care?" Here's why it reaches further than you'd think.

If you have a pension or index fund, you're probably exposed whether you chose to be or not. Microsoft, Nvidia, and Oracle are among the largest companies in most index funds. If the AI bet wobbles, ordinary retirement savings feel it. That's the quiet way this story touches almost everyone.

If you're early in your career — especially in white-collar or tech work — the pressure point is real but specific. The trillion-dollar bet ultimately depends on businesses extracting enough value from AI to justify it, and at enterprise scale that value often comes from needing fewer people for the same output. The effect tends to land hardest on entry-level roles — the very tasks that used to be how juniors cut their teeth. It's not mass overnight replacement; it's a rising bar and a thinner bottom rung.

If you use AI tools daily, enjoy the prices while they last. A lot of today's cheap, powerful AI is subsidised by investor money — sold below true cost to capture market share. The leak shows the pressure to actually turn a profit is now arriving. Expect prices to rise and free tiers to shrink over time.

And here's the part I'd genuinely encourage you to sit with, because it's where opportunity lives. When AI compresses generalist knowledge work, the roles that hold their value are the ones where judgement, trust, accountability, and security matter — work where being wrong has real consequences and a human has to own the outcome. That's not a coincidence. It's structural. If you're choosing where to invest your learning, that's the defensible ground.

What We Genuinely Don't Know

In the spirit of being straight with you, here's what remains uncertain — because anyone telling you they're sure about this is selling something.

- The leaked figures, while verified by the Financial Times and reported across many outlets, are a snapshot. Audited statements are credible, but the projections built on them (the $200B-by-2030 target) are forecasts, not facts.

- Several of the "circular" deal figures are commitments, letters of intent, or "up to" numbers — not deployed cash. Nvidia's "$100 billion" is announced intent in tranches. Stargate's "$500 billion" is a target. Treat the headline aggregates with appropriate caution.

- Whether this is a bubble is, by definition, only knowable in hindsight. Credible, serious people are on both sides. The bear case (artificial demand, systemic risk) and the bull case (real usage, solvent players) are both internally coherent right now.

The Bottom Line

OpenAI isn't quietly dying — its revenue is exploding and its IPO is coming. But it has placed one of the largest bets in business history: roughly a trillion dollars of compute, structured through a web of deals so interlinked that serious economists are using the word "bubble." The scary loss headline is mostly accounting noise. The genuine risk sits off the balance sheet, in commitments that assume the AI growth story stays true.

For the rest of us, the lesson isn't to panic — it's to position. Whatever happens to OpenAI's share price, the durable human ground in an AI economy is the work that can't be wrong without consequence: judgement, trust, and security. That's the bet I'd make.

OpenAI Finances FAQ

Did OpenAI really lose $38.5 billion in 2025?

On paper, yes — but around $41.55 billion of that figure is a one-time, non-cash accounting charge from its non-profit-to-for-profit conversion (a fair-value remeasurement of convertible interests and warrant liabilities). It reflects real dilution for stakeholders, but it is not cash burning out the door. The real economic loss is closer to the $20.92 billion operating loss, and lower still on a pure cash basis.

How much revenue does OpenAI make?

OpenAI reported $13.07 billion in revenue in 2025, up from $3.7 billion in 2024 — roughly triple year on year, according to leaked audited figures independently verified by the Financial Times.

What is "circular financing" in AI?

It is when the same companies that sell OpenAI its compute — Nvidia, Microsoft, Oracle — also invest in OpenAI, so money flows in a loop. Critics warn it can inflate apparent demand and create systemic risk: if OpenAI cannot pay Oracle, Oracle cannot pay Nvidia. Defenders note the compute is real and the deals are not fraudulent round-tripping.

Is the AI industry a bubble?

Nobody knows for certain — that is only provable in hindsight. Serious analysts at the Wall Street Journal, Yale, and Bloomberg have flagged classic bubble warning signs, while defenders point out today's AI players are mostly profitable, solvent companies with real demand and strong balance sheets, unlike the dot-com startups of 2000.

Should I worry about my job because of OpenAI?

Not in a panic sense. The likely effect is gradual: pressure on entry-level and generalist knowledge work rather than overnight mass replacement. The most defensible roles are those requiring judgement, accountability, and security — work where being wrong has real consequences and a human has to own the outcome.

About the Author

Nathan House, Founder & CEO of StationX

Nathan House has 30 years of hands-on cybersecurity experience and is Cambridge-educated, holding CISSP, CISA, CISM, OSCP, CEH, and SABSA. He founded StationX in 1999 — one of the UK’s first cybersecurity companies — and has secured £71 billion in UK mobile banking transactions and the London 2012 Olympics, advising clients including Microsoft, Cisco, BP, Vodafone, and VISA. He authored the world’s most popular cybersecurity course — a #1 Udemy bestseller taken by over 500,000 students — and was named Cyber Security Educator of the Year 2020, AI Security Educator of the Year, and a UK Top 25 Security Influencer 2025. A DEF CON speaker and featured expert on CNN, Fox News, NBC, and the BBC, Nathan leads StationX’s training of more than half a million students worldwide.